Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. We follow strict ethical journalism practices, which includes presenting unbiased information and citing reliable, attributed resources. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Before making adjustments, it is important to understand first what adjustments are and why they are needed.

- In the accounting cycle, adjusting entries are made prior to preparing a trial balance and generating financial statements.

- Under the accrual basis of accounting, revenues are recorded at the time of delivering the service or the merchandise, even if cash is not received at the time of delivery.

- Adjustment entries are important accounting tools that help businesses to accurately record their financial transactions and ensure that their financial statements are accurate.

- For example, if a company has recognized revenue that has not yet been earned, an adjustment entry is made to remove this revenue from the income statement.

Unearned Revenues

Adjusting Entries refer to those transactions which affect our Trading Account (profit and loss account) and capital accounts (balance sheet). Closing entries relate xero authentication on buffalo app exclusively with the capital side of the balance sheet. Some transactions may be missing from the records and others may not have been recorded properly.

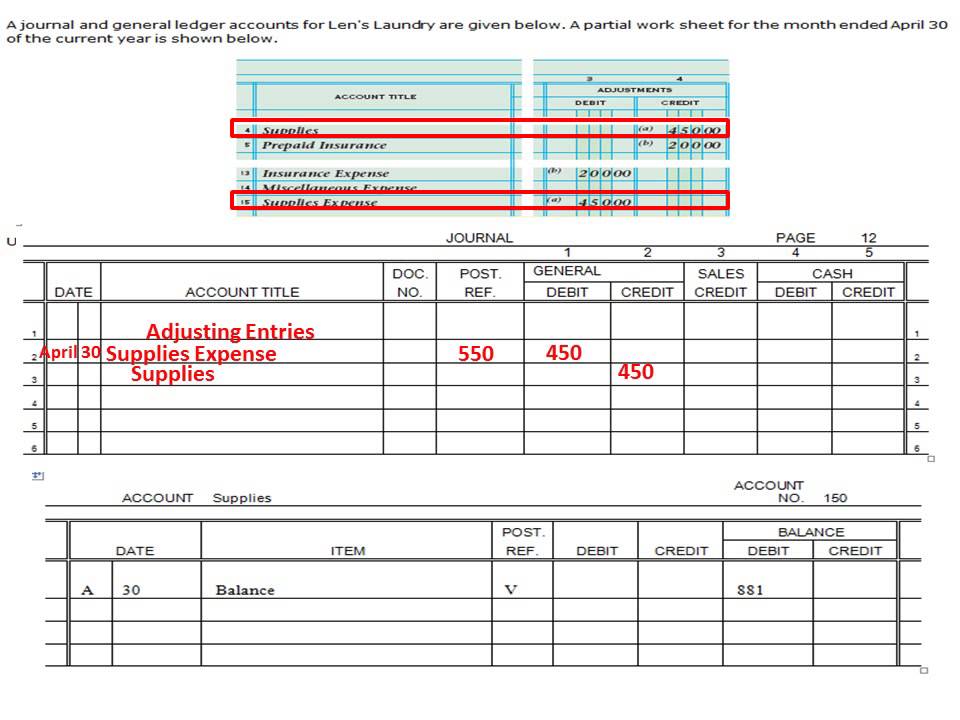

Adjusting Journal Entry: Definition, Purpose, Types, and Example

If you don’t adjust your adjusting entries, your balance sheets may be inaccurate. That includes your income statements, profit and loss statements and cash flow ledgers. An adjusting journal entry involves an income statement account (revenue or expense) along with a balance sheet account (asset or liability). It typically relates to the balance sheet accounts for accumulated depreciation, allowance for doubtful accounts, accrued expenses, accrued income, prepaid expenses, deferred revenue, and unearned revenue. Businesses sometimes fail to properly adjust for prepaid expenses or unearned revenues. However, as of December 31 only one month of the insurance is used up.

Deferred revenues

T-accounts will be the visual representation for the Printing Plus general ledger. That’s why most companies use cloud accounting software to streamline their adjusting entries and other financial transactions. Manually creating adjusting entries every accounting period can get tedious and time-consuming very fast. At the same time, managing accounting data by hand on spreadsheets is an old way of doing business, and prone to a ton of accounting errors.

An adjusting journal entry is typically made just prior to issuing a company’s financial statements. Income statement accounts that may need to be adjusted include interest expense, insurance expense, depreciation expense, and revenue. The entries are made in accordance with the matching principle to match expenses to the related revenue in the same accounting period. The adjustments made in journal entries are carried over to the general ledger that flows through to the financial statements. Sometimes companies collect cash from their customers for goods or services that are to be delivered in some future period. Such receipt of cash is recorded by debiting the cash account and crediting a liability account known as unearned revenue.

Every time a sales invoice is issued, the appropriate journal entry is automatically created by the system to the corresponding receivable or sales account. Now that we know the different types of adjusting entries, let’s check out how they are recorded into the accounting books. These prepayments are first recorded as assets, and as time passes by, they are expensed through adjusting entries. When you make adjusting entries, you’re recording business transactions accurately in time.

Adjusting entries update previously recorded journal entries, so that revenue and expenses are recognized at the time they occur. Our visual tutorial for the topic Adjusting Entries shows you how every adjusting entry will impact both the balance sheet and the income statement. The balance sheet reports the assets, liabilities, and owner’s (stockholders’) equity at a specific point in time, such as December 31. The balance sheet is also referred to as the Statement of Financial Position.

This principle only applies to the accrual basis of accounting, however. If your business uses the cash basis method, there’s no need for adjusting entries. At first, you record the cash in December into accounts receivable as profit expected to be received in the future.

Be the first to post a comment.