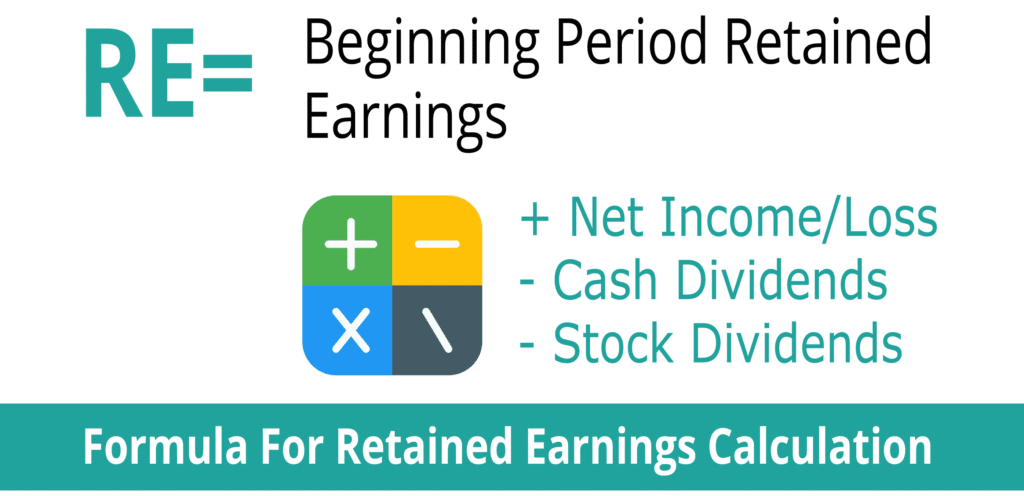

Retained earnings are calculated by subtracting a company’s total dividends paid to shareholders from its net income. This gives you the amount of profits that have been reinvested back into the business. The retained earnings (or retention) ratio refers to the amount of earnings retained by the company compared to the amount paid to shareholders in dividends.

How confident are you in your long term financial plan?

- In this case, the present value of cash flows is $198.61 million, and each share is worth $3.97.

- Negative retained earnings can signal to stakeholders that a company’s financial position is weakening, which may affect their decisions and perceptions.

- Though cash dividends are the most common payout, remember that stock dividends are another option.

- Sum all costs your company incurs, including cost of goods sold, salaries, rent, and other operating expenses.

- Strategic decisions, such as aggressive expansion or acquisitions, can also contribute to negative retained earnings.

- Movements in a company’s equity balances are shown in a company’s statement of changes in equity, which is a supplementary statement that publicly traded companies are required to show.

In between the opening and closing balances, the current period net income/loss is added and any dividends are deducted. The potential implications of a negative retained earnings balance depend on the severity and duration of the losses. In the short term, negative retained earnings may decrease shareholder confidence and make it more difficult for the company to obtain financing. In the long term, negative retained earnings may indicate that a company is not financially viable and may lead to its eventual failure. If a company has a net loss for the accounting period, a company’s retained earnings statement shows a negative balance or deficit.

AccountingTools

Shareholder equity represents the amount left over for shareholders if a company pays off all of its liabilities. To see how retained earnings impact shareholders’ equity, let’s look at an example. Negative retained earnings often arise from a company’s prolonged inability to generate a profit, which can be due to a variety of operational or external factors. For example, a business may experience a downturn in sales due to increased competition, leading to reduced revenue and, consequently, losses.

Step 1 of 3

The details are up to you, and you should use what you’ve learned here to make smart decisions regarding retained earnings and the future of your business. You can stay on top of your earnings, get accurate reports, and easily track transitions with QuickBooks. The loss might be insignificant, but the retained earnings could have been already reinvested or paid out to the shareholders, so there is nothing or too little left in the account. Some benefits of reinvesting in retained earnings include increased growth potential and improved profitability. Reinvesting profits back into the business can help it expand and become more successful over time.

Valuing Companies With Negative Earnings

Retained earnings can be used to pay off existing outstanding debts or loans that your business owes. CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. negative retained earnings CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

Which of these is most important for your financial advisor to have?

Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative. Additional paid-in capital is included in shareholder equity and can arise from issuing either preferred stock or common stock. The amount of additional paid-in capital is determined solely by the number of shares a company sells.

There is no change in the shareholder’s when stock dividends are paid out, however, you’ll need to transfer the amount from the retained earnings part of the balance sheet to the paid-in capital. The amount transferred to the paid-in capital will depend upon whether the company has issued a small or a large stock dividend. Creditors and lenders may also reassess their relationship with a business displaying negative retained earnings. They might perceive the company as a higher credit risk, which could lead to more stringent borrowing terms or a reluctance to extend further credit. This can hamper the company’s ability to finance operations or invest in growth opportunities, potentially leading to a downward spiral of financial health.

These reduce the size of a company’s balance sheet and asset value as the company no longer owns part of its liquid assets. Cash payment of dividends leads to cash outflow and is recorded in the books and accounts as net reductions. As the company loses ownership of its liquid assets in the form of cash dividends, it reduces the company’s asset value on the balance sheet, thereby impacting RE. They can be a red flag for investors, as they may indicate that the company is struggling financially and may not be able to generate sufficient profits in the future.

A summary report called a statement of retained earnings is also maintained, outlining the changes in RE for a specific period. Retained earnings are a type of equity and are therefore reported in the shareholders’ equity section of the balance sheet. Although retained earnings are not themselves an asset, they can be used to purchase assets such as inventory, equipment, or other investments. Therefore, a company with a large retained earnings balance may be well-positioned to purchase new assets in the future or offer increased dividend payments to its shareholders. The retained earnings equation is a fundamental accounting concept that helps companies calculate the amount of profit that is kept in the business after dividends are distributed to shareholders.

These funds can be used for anything the business chooses, including research and development, buying new equipment, or anything else that will lead to growth for the company. Retained earnings encompass all earnings retained by the company, whether they come from core business operations, one-time windfalls, or investment gains. It’s vital to differentiate between these sources of earnings when assessing a company’s financial strategy and sustainability. The RE balance may not always be a positive number, as it may reflect that the current period’s net loss is greater than that of the RE beginning balance.

Retained earnings are usually considered a type of equity as seen by their inclusion in the shareholder’s equity section of the balance sheet. Though retained earnings are not an asset, they can be used to purchase assets in order to help a company grow its business. The significance of retained earnings lies not only in what they represent but also in their potential impact on strategic decision-making within an organization. Negative retained earnings may necessitate a reevaluation of operations, investment strategies, and even management practices. Stakeholders from investors to employees keep a close watch on this metric as it often influences decisions at multiple levels of business operations.

Be the first to post a comment.